Bounce Back Loans six years on: the insolvency legacy still unfolding

Six years on from the launch of the Bounce Back Loan Scheme (BBLS), the story has moved well beyond emergency business support.

For many businesses, Bounce Back Loans (BBLs) were a genuine lifeline. They were introduced quickly, distributed at scale and designed to help small businesses survive a period of acute and unprecedented uncertainty. That should not be lost in any analysis. The scheme was created in extraordinary circumstances, and many directors used the funds responsibly to protect jobs, manage cash flow and keep their businesses trading.

The legacy, however, is a little more complex. The BBLS has become one of the clearest examples of what can happen when urgent financial support, limited verification and weak early safeguards combine. The result is still being seen in repayment pressure, director disqualifications, insolvency investigations, criminal proceedings, public loss and recovery action.

“More than 1.56 million BBLs were approved, with a total approved value of £47.36 billion”.

The original purpose of the BBLS

The scheme launched in May 2020. It allowed small and medium sized businesses to borrow between £2,000 and £50,000, up to a maximum of 25% of annual turnover. Loans were fully backed by a 100% government guarantee, with no capital repayments due in the first year and a fixed interest rate of 2.5%.

It was intended to be simple and quick. Businesses were facing immediate pressure and the government wanted to get money into the economy at pace.

By July 2021, final government figures showed that more than £47 billion had been approved through the BBLS alone. Across the wider emergency loan schemes, almost £80 billion of government backed lending was delivered during the pandemic, including the BBLS, the Coronavirus Business Interruption Loan Scheme and the Coronavirus Large Business Interruption Loan Scheme.

The British Business Bank’s Year 3 evaluation of those three Covid loan guarantee schemes found that they may have prevented hundreds of thousands of business closures and protected up to 3.5 million jobs. It also found an overall economic benefit of £77 billion across the scheme.

It’s important to mention these stats because the scheme should not be reduced to solely a story of fraud and misuse. The support did have a real economic purpose and many businesses did exactly what they were supposed to do with the loans.

IG Commentary

“ Bounce Back Loans supported many businesses at a time when they had few other options. The issue is that the same features that made the scheme accessible also made it vulnerable. The insolvency legacy is now revealing where that line was crossed.”

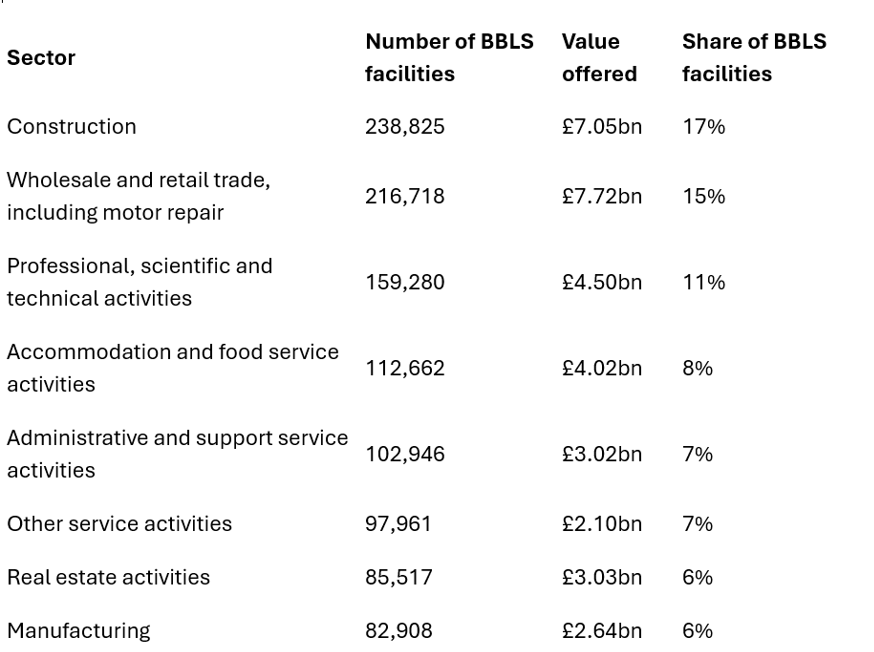

Which sectors benefitted most from the BBLS

The scheme was used widely across the economy, but some sectors drew particularly heavily on it. British Business Bank data showed that construction received the highest number of BBLS facilities, accounting for 17% of loans offered. Wholesale and retail followed at 15%, and received the highest total value of BBLS lending, at £7.72bn. Accommodation and food services accounted for 8% of facilities, reflecting the pressure placed on hospitality and leisure businesses during repeated restrictions during COVID.

NB: The figures are not the final scheme totals, as the data was taken in January 2021 before the scheme closed in March 2021

Where the risk entered the system

The National Audit Office (NAO) identified the central problem in its 2021 update. The Government had prioritised payment speed over almost all other aspects of value for money. The scheme relied heavily on self-certification – in practice this meant that businesses were asked to confirm key details themselves, including turnover and eligibility, with limited upfront verification. Credit and affordability checks were removed. Counter fraud measures were introduced, but many came too late to prevent abuse.

At that stage, the NAO referred to a “most likely” estimate of £4.9 billion of fraudulent loans, although it also stressed that the true level would become clearer over time.

That forecast has since been overtaken by wider public sector fraud analysis. In December 2025, the Covid Counter Fraud Commissioner’s final report found that taxpayers had lost £10.9 billion to fraud and error across Covid support schemes. Bounce Back Loans were specifically identified as one of the schemes rolled out with high fraud risks and insufficient early safeguards.

“£10.9 billion was lost to fraud and error across Covid support schemes.”

Covid Counter Fraud Commissioner, December 2025

The latest repayment picture

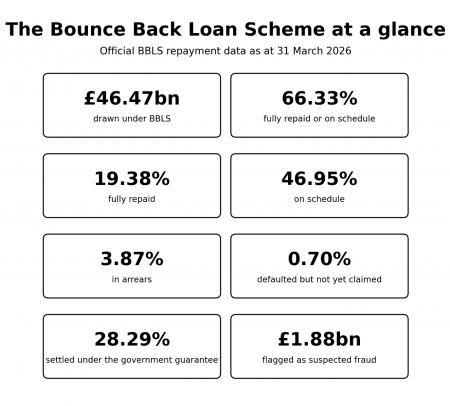

The most up to date official repayment data, published in 2026 and showing the position as at 31 March 2026, gives a more detailed view of where the scheme now stands.

Businesses had drawn £46.47 billion under the BBLS. By volume, 66.33% of facilities were either fully repaid or on schedule. That includes 19.38% fully repaid and 46.95% on schedule.

At the same time, 3.87% of facilities were in arrears, while 0.70% were defaulted but had not yet progressed to lender claims. The government guarantee had been settled on 28.29% of total BBLS facilities by volume.

Lenders had also flagged £1.88 billion of the £46.47 billion drawn value as suspected fraud. Of the £11.82 billion total settled amount as at 31 March 2026, £1.58 billion had been paid out to lenders against loans carrying a suspected fraud flag.

Source: HM Treasury and British Business Bank COVID loan guarantee schemes repayment data March 2026

Source: HM Treasury and British Business Bank COVID loan guarantee schemes repayment data March 2026

These figures create a more balanced picture. A large proportion of borrowers are repaying or have repaid. At the same time, the scale of suspected fraud, defaults and guarantee settlements means the BBLS is still a highly contentious issue.

There is no single official figure showing how many BBL borrowers are still trading successfully six years on. Government data does show that, by 31 March 2025, more than 113,000 companies that had taken out a Bounce Back Loan had either been dissolved or entered insolvent liquidation.

What replaced Bounce Back Loans?

The BBLS closed to new applications and top ups on 31 March 2021. It was followed by the Recovery Loan Scheme, which supported access to finance as businesses moved out of the immediate pandemic period.

From 1 July 2024, the Recovery Loan Scheme was extended and rebranded as the Growth Guarantee Scheme.

The Growth Guarantee Scheme is now the main government backed debt finance scheme for smaller UK businesses. It is designed to support access to finance for businesses looking to invest and grow, rather than provide emergency rescue funding.

So whilst BBLs were crisis lending, the current support landscape is more conventional, more lender led and more focused on viable businesses with a clear proposition.

Under the Growth Guarantee Scheme, facilities can generally be provided up to £2 million per business group, with products including term loans, overdrafts, asset finance, invoice finance and asset-based lending. The government provides lenders with a 70% guarantee, but the borrower remains 100% liable for the debt. Businesses can use the finance for legitimate business purposes, including managing cash flow and investment, but they must be able to afford the additional borrowing.

IG commentary

“The replacement schemes tell their own story. The emergency phase has passed. Businesses looking for finance now need to show viability, affordability and a credible plan. That is a very different environment from the early months of the pandemic.”

What support is available to businesses now?

There are still support options available to UK businesses, although none are a direct like for like replacement for BBLs.

The Growth Guarantee Scheme is the closest successor for businesses seeking government backed finance. It may be relevant for viable businesses looking to invest, manage working capital, purchase assets or support growth, subject to lender approval.

Businesses that already have BBLs may still be able to use Pay As You Grow options to manage repayments. These can include extending the loan term to ten years, moving temporarily to interest only repayments or taking a repayment holiday, depending on the circumstances and lender process.

Start Up Loans remain available for newer businesses and entrepreneurs. These can provide personal loans for business purposes, alongside mentoring and support.

There are also regional and national finance routes delivered through the British Business Bank and other public bodies, including investment funds aimed at different parts of the UK. Government grant funding can be searched through the Find a Grant service, and broader business support is now being signposted through Business.gov.uk.

For leadership and management development, Help to Grow: Management remains available for eligible SME leaders. It is designed to improve management capability and productivity, with the course substantially government funded.

The practical message for directors is that finance is still available, but the environment has changed. The focus now is on sustainable borrowing, affordability and proper use of funds.

The Growth Guarantee Scheme generally supports facilities of up to £2 million, with a 70% government backed guarantee to lenders.

IG Commentary

“Directors should be cautious about taking on further borrowing to manage existing pressure without first understanding the company’s financial position. New finance can support recovery and growth, but it can also deepen the problem if the underlying business is no longer viable.”

Director conduct and the insolvency consequences

For directors, the key point here is simple: emergency funding such as the BBLS did not suspend directors’ duties.

BBLs still had to be repaid. They were not to be used for personal purposes. Official guidance makes clear that misconduct can include providing false information on a loan application, using the loan for personal benefit or dissolving a company to avoid repayment. The potential consequences include winding up, director disqualification and compensation orders.

That is where the insolvency implications become most significant.Once a company enters liquidation, administration or dissolution scrutiny, the use of a BBL can become part of the wider review of director conduct. Questions may include whether the company was entitled to the loan, whether the turnover declared was accurate, whether the money was used for the benefit of the business, whether creditors were treated properly and whether records support the director’s decisions.

IG Commentary

“The existence of a Bounce Back Loan is not, in itself, evidence of wrongdoing. The problem comes when the paper trail does not support the application, the use of funds or the decisions taken when the company was already under pressure.”

A continuing enforcement story

The enforcement data shows that the consequences of misuse are still happening today:

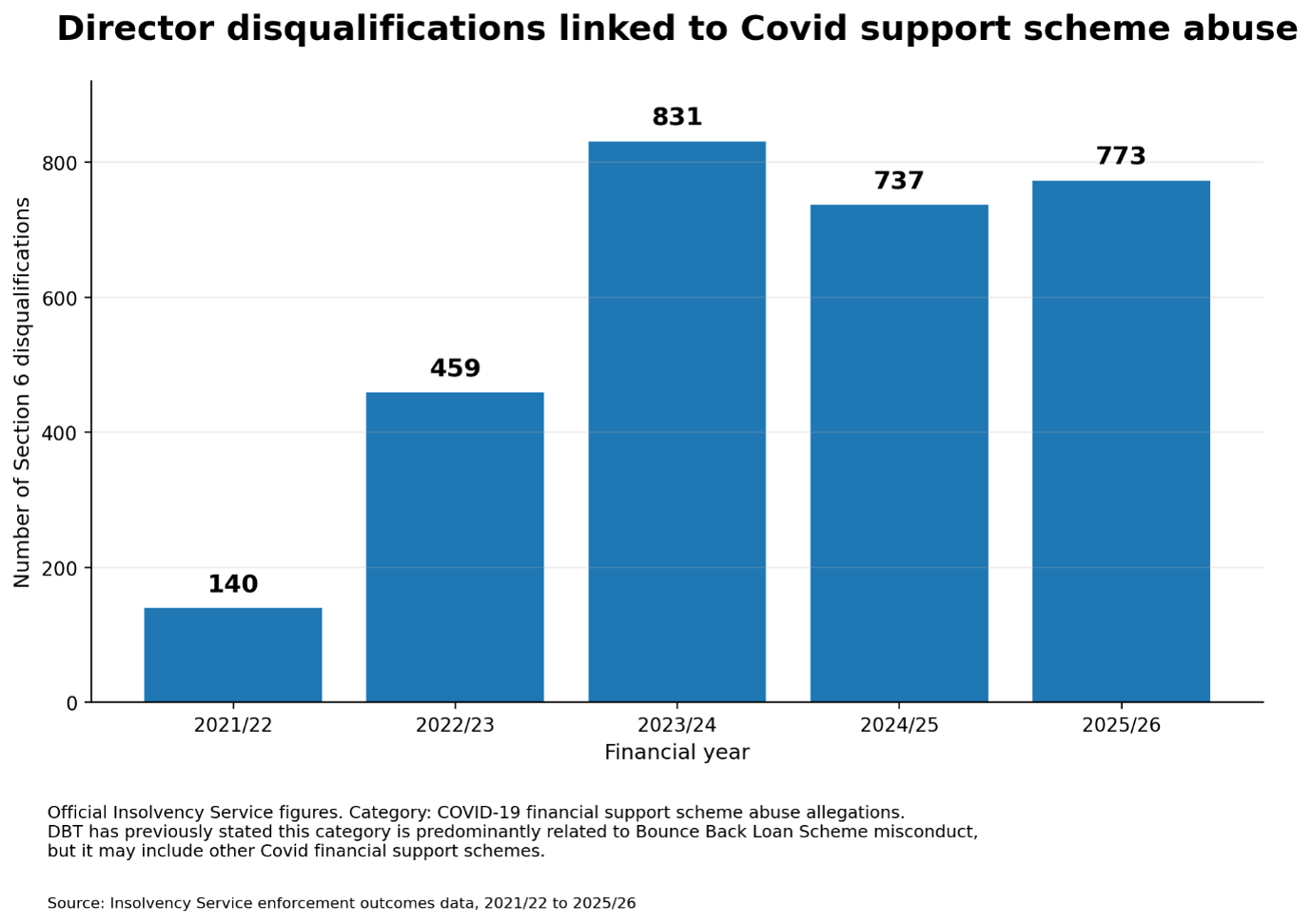

In 2025 to 2026, the Insolvency Service recorded 1,153 director disqualifications in Great Britain resulting from its enforcement activity. Of the Section 6 disqualifications, 773 related to COVID-19 financial support scheme abuse allegations. The average ban for those Covid related allegations was 9.4 years.

Official Insolvency Service data shows that disqualifications involving COVID-19 financial support scheme abuse allegations rose sharply after 2021 to 2022 and remained high through to 2025 to 2026. The category is predominantly related to BBLS, but may include other Covid financial support schemes.

The wider enforcement picture also includes bankruptcy and debt relief restrictions, criminal convictions and compensation orders. In 2025 to 2026, Insolvency Service data recorded 77 defendants convicted following criminal investigations, 31 of which related to COVID-19 financial support scheme abuse.

IG Commentary

“The enforcement trend is a reminder that the Insolvency Service is still actively pursuing pandemic support abuse. Directors who assume these matters have gone quiet because the scheme closed in 2021 may be badly mistaken.”

Recent cases show the range of conduct still being pursued

Recent enforcement activity shows that BBL issues are still being pursued across a wide range of factual scenarios. The most serious cases involve deliberate fraud, but the wider pattern includes inflated turnover, duplicate applications, companies that had never traded, personal use of funds and directors acting while disqualified.

These examples show why BBLs remain relevant to insolvency and director conduct work six years on.

Multiple companies and personal spending

In May 2026 The Times reported that Steven Brookes, a company director from Cornwall, admitted fraud offences after securing £300,000 in Covid Bounce Back Loans. According to the report, the loans were obtained by inflating turnover figures and making applications across several companies, including companies said to have never traded. The funds were allegedly used for personal spending, with the Insolvency Service now seeking recovery under the Proceeds of Crime Act.

Company never traded

In May 2026, Ademilson Nascimento was banned for the maximum period of 15 years after securing £46,500 in Bounce Back Loan funds for a construction company which had never traded.

Multiple loans and acting while disqualified

In April 2026, Matloob Hussain was jailed after applying for three Covid Bounce Back Loans he was not entitled to and acting as a director while already disqualified.

Confiscation and recovery action

In January 2026, Zahid Afzal was ordered to repay almost £200,000 after fraudulently obtaining three £50,000 Bounce Back Loans for mobile phone companies, including by falsely declaring that previous loans had not been received, inflating turnover and transferring funds to personal accounts.

False turnover and imprisonment

In October 2025, Craig Smith, the director of a property maintenance company, was jailed after falsely claiming a £50,000 Bounce Back Loan using turnover figures that did not reflect the company’s position.

Second loan and criminal sentence

In January 2026, printing firm director Vishal Jobanputra received an 18 month suspended sentence, was disqualified for three years and fined after fraudulently obtaining a second Covid loan.

Personal spending

In July 2025, the Insolvency Service reported that Junaid Dar had fraudulently received three Bounce Back Loans and diverted significant sums for personal spending, including restaurants, safari park spending and personal credit card debt.

IG Commentary

“The most serious cases attract headlines, but the underlying issues are broader. In many insolvency cases, the questions are less dramatic but still important. Was the company entitled to the loan? Was the money used properly? Were creditors prejudiced? Can the director evidence what happened?”

The lesson for directors

The retrospective lesson is not that every business which took a BBL should be concerned. Many borrowed legitimately, used the money properly and continue to repay.

The lesson is that directors need to understand how these loans are viewed when a business later fails.

Where a company is insolvent or approaching insolvency, directors must consider the interests of creditors. They must keep proper records. They must avoid preferring some creditors unfairly. They must not treat company money as personal money. They must take advice before dissolving a company with outstanding liabilities or before making decisions that could later be challenged.

In practical terms, the key evidence is often straightforward. Directors should be able to explain the basis of the original application, the turnover figure used, how the funds were spent, what the company’s financial position was at the time and what advice was taken.

A lack of records may make an already difficult situation worse.

What have BBLs taught us?

Six years on, the lesson from BBLs is not simply that emergency funding can be abused. It is that decisions made quickly in a crisis can leave a long legal, financial and evidential tail:

Here’s our summary of the lessons learnt:

1.Speed and scrutiny need to be better balanced

BBLs showed that government support can be delivered quickly and at scale. They also showed that speed without enough upfront verification can create problems that take years to investigate, recover and resolve.

2. Self-certification has limits

Trusting applicants to confirm eligibility, turnover and trading status helped money reach businesses quickly. It also created opportunities for inflated figures, duplicate applications and loans to companies that were not entitled to support.

3.Company debt can become a director conduct issue

An unpaid BBL does not automatically make a director personally liable. In most cases, it remains a company debt. The risk arises where the application was false, the money was used personally, or the company was later handled in a way that prejudiced creditors.

4. Records matter long after the crisis has passed

Directors may now be asked to explain decisions made in 2020 or 2021. Those with clear records showing why the loan was taken, how the figure was calculated and how the money was spent will be in a much stronger position.

5. Rescue finance is not a substitute for insolvency advice

Borrowing can help a viable business survive a temporary shock. It can also delay difficult decisions and increase creditor losses if the underlying business is no longer sustainable. Taking advice early remains one of the most important steps a director can take.

Sources used

National Audit Office, The Bounce Back Loan Scheme: an update, December 2021

HM Treasury and British Business Bank, COVID-19 loan guarantee schemes repayment data: March 2026

HM Treasury, Covid fraud cost UK taxpayer £10.9 billion, December 2025

Covid Counter Fraud Commissioner, Pursuing Recoveries and Preventing Reoccurrence, Final Report, December 2025

British Business Bank, Evaluation of the COVID-19 Loan Guarantee Schemes Year 3 Report, May 2025

HM Treasury, Final Covid loans data reveals £80 billion of government support through the pandemic, July 2021

British Business Bank, Bounce Back Loan Scheme legacy programme information

British Business Bank, Recovery Loan Scheme legacy programme information

British Business Bank, Growth Guarantee Scheme information

British Business Bank, Start Up Loans information

GOV.UK, Find a Grant service

GOV.UK, Business finance and support finder

GOV.UK, Help to Grow: Management

GOV.UK, Bounce Back loans held by dissolved or liquidated companies, June 2025

Insolvency Service, Enforcement Outcomes 2025 to 2026