Retail Insolvency and the UK High Street Reset

Reflections on the changing face of the UK high street

Over the past two decades the UK high street has undergone one of the most significant structural transformations in modern retail history. Major national chains have disappeared, consumer behaviour has shifted toward online shopping, and operating costs have increased sharply for physical retailers.

At the same time, insolvency activity within the retail sector has remained persistently high. Some brands have collapsed entirely, others have shrunk their store estates, and a smaller number have successfully adapted to a very different retail environment.

This article explores how the high street has evolved, which retailers have disappeared, which have survived, and what the future may hold. It also considers what these changes mean from a retail insolvency and restructuring perspective, particularly for directors, creditors and businesses facing financial pressure.

Key takeaways

- The UK high street is experiencing a long-term structural reset rather than a short-term downturn.

- Retail insolvency levels remain elevated, with rising employment and property costs continuing to put pressure on margins.

- Many retailers now pursue restructuring, administration or CVAs rather than disappearing immediately.

- Early legal and restructuring advice can help preserve more options for struggling businesses.

1. Setting the scene: the numbers behind the change

The transformation of the high street has been gradual rather than sudden. Retail closures have been a consistent feature of the landscape in recent years. In 2024, 12,804 chain stores closed across Great Britain, while 9,002 opened, resulting in a net loss of around 3,800 stores. The trend continued through 2025, with more than 13,000 chain store closures recorded across the year, reinforcing the long-term contraction of physical retail.

Retailers are also facing sustained cost pressure. From April 2025, the National Living Wage increased to £12.21 per hour. From April 2026, it rose again to £12.71, adding further pressure to payroll costs. Employer National Insurance changes and threshold adjustments have also increased the overall cost of employment.

The business rates landscape has also shifted. From April 2026, a revised system applies, including lower multipliers for qualifying retail, hospitality and leisure premises below a £500,000 rateable value threshold. While this offers some support for smaller occupiers, many larger high street premises continue to face relatively high rates liabilities, particularly in prime locations.

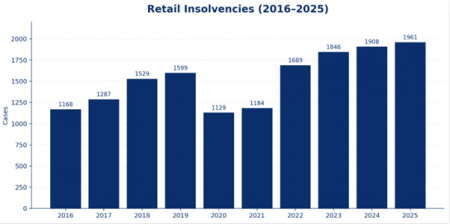

The insolvency environment remains elevated. England and Wales recorded 23,938 company insolvencies in 2025, including 1,961 in the retail sector alone and 3,728 across wholesale and retail combined. Early 2026 data shows insolvency levels remain high, with retail continuing to represent a significant share of overall cases.

Another structural shift has been the withdrawal of banks from town centres. More than 6,600 bank branches have closed since 2015, removing a key source of routine footfall.

Taken together, these figures show that the high street is not experiencing a short-term downturn. It is undergoing a long-term structural reset. For many retailers, that reset has translated into sustained financial stress, tighter margins and greater reliance on formal or informal restructuring options.

Retailers facing creditor pressure, rent arrears or HMRC debt may reach a point where early insolvency and restructuring advice becomes essential.

IG commentary:

"Retail insolvencies tend to follow a recognisable pattern. Rising staff costs, higher property overheads, declining footfall and legacy store estates combine over time, increasing pressure across the business. That pressure is rarely driven by a single event. More often, we see a cumulative build-up across the creditor base, including HMRC arrears, rent liabilities and supplier pressure. Once those factors align, the available restructuring options narrow quickly."

2. High street staples that have disappeared or retreated

Twenty years ago most British towns had a similar retail mix. Large national chains dominated the high street and acted as anchor tenants.

Many of those names have now disappeared or significantly reduced their presence.

Major retailers that have disappeared or materially retreated

- Woolworths – collapsed in 2008

- BHS – collapsed in 2016

- Debenhams – stores closed in 2021, brand now online

- House of Fraser – survived with significantly reduced estate

- Comet – collapsed in 2012

- Maplin – collapsed in 2018, later revived online

- Phones 4U – collapsed in 2014

- Toys R Us UK – collapsed in 2018

- Blockbuster – closed following streaming disruption

- Borders – closed UK stores

- Wilko – entered administration in 2023, brand partially revived

More recent casualties and restructurings include:

- The Body Shop – UK administration in 2024

- Ted Baker – UK retail administration and store closures in 2024

- The Original Factory Shop – administration in January 2026

- Quiz – administration process in early 2026

The disappearance or reduction of these retailers has removed many of the anchor tenants that historically drove footfall.

Large department stores and variety retailers once occupied significant space. Their loss has left many high streets with large vacant units that are difficult to repurpose, weakening the surrounding retail environment. In many cases, the loss of anchor tenants does not simply affect landlords and consumers. It can also increase pressure on neighbouring retailers, creditors and local supply chains.

IG commentary

"The loss of anchor stores has a ripple effect. When department stores, banks or large-format retailers leave, footfall drops and neighbouring businesses often struggle. That increases the likelihood of further restructurings and insolvencies.”

3. Retailers that have shown resilience

Despite widespread disruption, a number of retailers have adapted successfully.

The most resilient businesses tend to fall into three categories.

Discount retailers

- B&M – rapid national expansion

- Home Bargains – continued growth

- Poundland – still a major presence, though actively restructuring and reducing its estate

Large format destination retailers

- Primark – strong performer on major high streets

- JD Sports – continued expansion

Primark continues to attract significant footfall due to its scale, pricing and in-store experience.

Specialist retailers

- Robert Dyas – hardware and home

- Ryman – stationery

- Waterstones – books

- The White Company – premium lifestyle

- White Stuff – fashion

- Hotel Chocolat – premium gifting

Ryman and Robert Dyas benefit from group backing, providing operational scale and resilience.

IG commentary

“The most resilient retailers tend to share common traits: a clear commercial proposition, operational flexibility and often the backing of a wider group structure. From a restructuring perspective, these characteristics enable businesses to adjust their cost base more quickly and maintain access to funding on more favourable terms as trading conditions evolve.”

4. Restructuring rather than disappearance

Not all struggling retailers disappear completely. Many brands survive following acquisition, partnership or restructuring.

Examples include:

- Paperchase – brand acquired by Tesco

- Joules – acquired by Next

- Debenhams – online brand acquired by Boohoo

- Topshop – acquired by ASOS

- FatFace – majority stake acquired by Next

- Gap – UK business retained via Next partnership and later physical return

- Superdry – court-approved restructuring in 2024

This highlights a growing trend. Even where store estates collapse, brand value can survive and be redeployed in a different format.

Depending on the circumstances, restructuring options may include a Company Voluntary Arrangement, administration, asset sales, consensual landlord negotiations or, where rescue is no longer viable, liquidation.

IG commentary

“Modern retail insolvencies frequently involve separating the viable elements of the business from the legacy structure. Intellectual property, online platforms and customer data are often preserved, while the physical estate is rationalised through formal processes.”

5. The shift away from traditional high streets

Retail geography has shifted significantly.

Many retailers now favour retail parks and out-of-town locations over secondary high street sites.

Recent data indicates:

- high street footfall continues to decline modestly year on year

- retail parks have shown comparatively stronger and more stable performance

- shopping centres sit between the two

Retail parks typically benefit from:

- convenient parking

- larger store formats

- easier logistics

- integration with online fulfilment

They also tend to maintain lower vacancy levels than many secondary high streets.

As a result, many retailers are consolidating into stronger locations while exiting weaker high street sites.

IG commentary

“Retail parks operate as property platforms rather than single businesses. Individual retailers may fail, but the location can remain viable if it continues to attract new tenants. That makes them structurally more resilient than many secondary high streets.”

6. The typical high street: then and now

A typical high street in 2008

- Department stores – Debenhams, BHS

- Variety retail – Woolworths

- Fashion – Topshop, Burton, Dorothy Perkins

- Electronics – Currys, Comet

- Books – WHSmith

- Household – Wilko

- Toys – Woolworths, Toys R Us

- Banking – Barclays, HSBC, Lloyds

A typical high street in 2026

- Discount retail – Poundland, B&M

- Health and beauty – Boots, Superdrug

- Food and drink – Greggs, Costa, Pret

- Specialist retail – Ryman, Robert Dyas

- Fashion anchors – Primark, JD Sports

- Services – barbers, nail salons, gyms

- Charity shops – increasingly common

- Wellness and healthcare – diagnostics, dental and performance services

The modern high street is more service-led and convenience-focused, with fewer large retail anchors.

IG commentary

“The shift toward service-led occupiers reflects a broader change in risk profile. Many of these businesses operate with lower stock exposure and more flexible cost structures, which can make them more resilient in periods of economic pressure.”

7. Retail insolvency trends over the last decade

Retail has consistently been one of the sectors most exposed to insolvency.

The overall trend has been one of sustained pressure, a temporary reduction during pandemic support, and then a renewed increase as support measures ended and cost inflation took hold.

Wholesale and retail combined exceeded 3,700 insolvencies in 2025, making it one of the largest distressed sectors.

IG commentary

“In retail insolvency work, the issue is often structural rather than sudden. Businesses built for a different era of footfall and store economics can struggle for years before a formal insolvency process becomes unavoidable. Since the withdrawal of pandemic support measures, HMRC has resumed a more active enforcement role. In many cases it is now a key creditor, and its position can be decisive in determining whether a restructuring proposal is viable.”

8. Retailers currently under pressure

Several well-known brands remain under pressure as they restructure or adapt to changing conditions.

- River Island – store closures and restructuring

- Poundland – ongoing restructuring and estate reduction

- TGJones – transition and repositioning following WHSmith high street sale

- Claire’s – UK administration, reflecting continued pressure in the accessories segment

- The Original Factory Shop – administration in January 2026

- Quiz – administration process in early 2026

These examples show that pressure remains widespread across the sector. For many retailers, the challenge is no longer whether change is required, but whether it can be implemented early enough to preserve the viable core of the business.

IG commentary

“Modern retail restructuring is usually about resizing. The aim is to preserve the viable core of the business while exiting loss-making locations and resetting the cost base. One of the recurring challenges in these situations is timing. Delayed action can reduce the range of available restructuring options, particularly where liabilities continue to accrue and creditor positions become more entrenched.”

9. What the future of the high street may look like

The high street is unlikely to return to its previous form.

Instead, it is evolving into a mixed-use environment incorporating:

- hospitality and leisure

- healthcare services

- residential development

- co-working space

- community uses

Retail will remain important, but is likely to occupy less space and serve a more defined role, often focused on convenience, experience and brand presence.

Stronger locations are likely to retain a core retail offering, while weaker high streets may continue to transition toward service-led and residential uses. For distressed retailers, that means future viability may depend less on scale alone and more on location quality, cost control and adaptability.

IG commentary

“The future high street will carry less traditional retail but a broader mix of uses. The dividing line will be between places that can successfully adapt and those that struggle to replace lost footfall. A central issue in many retail restructurings is the gap between operational viability and financial sustainability. The businesses that succeed over the long term are those able to align their cost base with the realities of modern trading conditions.”

10. Final Thoughts

The high street is unlikely to return to its previous form. Instead, it is moving toward a smaller, more selective and more service-led model.

Some retailers will continue to adapt successfully. Others will restructure, shrink or disappear. From an insolvency and restructuring perspective, the core challenge is no longer simply surviving a temporary downturn. It is adapting to a fundamentally different commercial environment.

For businesses facing cash flow pressure, creditor action, rent arrears or HMRC debt, early specialist advice can make a material difference to the options available, whether that involves restructuring, a CVA, administration or liquidation.

Sources

British Retail Consortium footfall data

The Insolvency Service company insolvency statistics

Which? bank branch closure tracker

Savills UK retail research

CBRE UK retail market outlook

JLL retail parks research

Reuters retail and restructuring reporting

This article is provided for general information only and does not constitute legal advice. For further guidance, please contact the team at Isadore Goldman.